On May 22, 2025, the U.S. House passed the One Big, Beautiful Bill Act (OBBBA), a sweeping legislative package that effectively repeals most clean energy provisions of the Inflation Reduction Act (IRA). Additionally, a key amendment that passed with the original OBBBA imposes two immediate eligibility conditions that disqualify the vast majority of clean energy projects currently under development. It also repeals core tax credits, reinstates pre-IRA limitations, and enacts aggressive restrictions on foreign-linked supply chains.

OBBBA is a budget reconciliation bill that scales back the Inflation Reduction Act’s clean energy provisions by introducing a narrower eligibility framework, time-bound credit availability, and technology-specific adjustments to federal support.

New Eligibility Requirements under OBBBA

The 60-Day Rule:

The final version of OBBBA introduces a dual-condition eligibility test for projects seeking to claim the new tech-neutral clean electricity tax credits (45Y and 48E). A project must meet both of the following:

- Begin construction within 60 days of the bill’s enactment, AND

- Be placed in service by December 31, 2028.

Definition of “Begin Construction”:

Failure to meet either condition results in complete disqualification from the credits, regardless of prior plans or compliance with IRA-era guidelines. Moreover, the definition of “In-service date” or “begin construction” remains aligned with IRS precedent. A project must either:

- Start physical work of a significant nature (on-site or off-site), or

- Incur at least 5% of total project costs and maintain continuous progress thereafter.

This dual requirement is not merely procedural; it is structural. By compressing the timeline to 60 days after enactment and enforcing a hard in-service deadline, the bill effectively excludes all but shovel-ready projects from eligibility.

The original version of OBBBA proposed an accelerated phase-down of the IRA’s tech-neutral Investment Tax Credit (48E) and Production Tax Credit (45Y). While the IRA tied the credit sunset to a 75% reduction in power sector greenhouse gas emissions from 2022 levels, OBBBA removed this emissions-based trigger entirely. Instead, it proposed a fixed phase-out beginning in 2029, with full expiration by 2032.

The amendment, however, eliminates both the IRA’s planned gradual step-down schedule (80%, 60%, 40%) through 2032 and OBBBA’s earlier accelerated timeline, while also removing the greenhouse gas emissions threshold. As a result, there is no glide path or transitional mechanism for delayed or phased projects-only a fixed sunset based on construction and in-service deadlines.

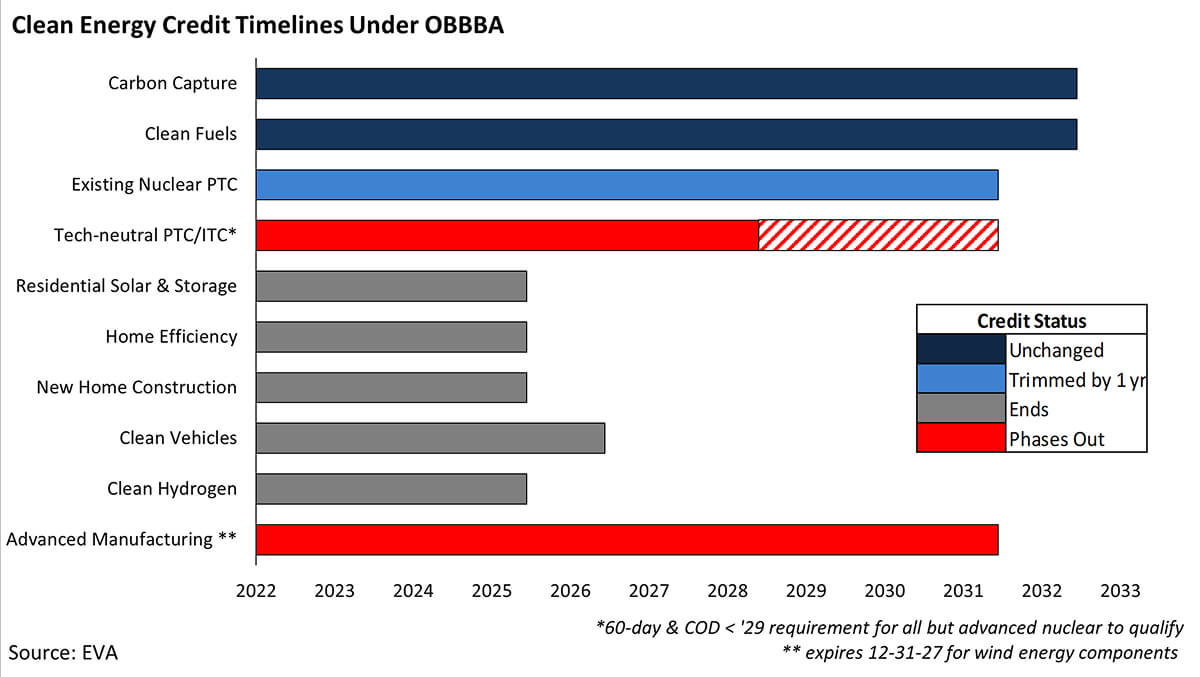

Termination and Restructuring of Clean Energy Tax Credits

The OBBBA delivers a sweeping contraction of the Inflation Reduction Act’s clean energy tax platform. In addition to imposing a 60-day construction start deadline and a December 31, 2028, in-service requirement, OBBBA accelerates the phase-out or eliminates nearly all major clean energy credits, with only a few strategic exceptions.

Credits Phased Out or Eliminated

- 45Y/48E (Tech-neutral clean electricity credits): Projects must begin construction within 60 days of enactment and be operational by the end of 2028 to qualify for the tax credits. Projects that miss either of these deadlines will no longer be eligible for the clean electricity PTC or ITC under the House proposal. No transitional glide path or partial credit is provided. Only new advanced nuclear projects are exempt from the 60-day construction start and pre-2029 in-service date requirements; they only need to meet the simpler construction start pre-2029 requirement to qualify for the credits and their subsequent phase-out.

- 25D* / 25C / 45L (Residential Incentives): Residential and consumer energy incentives, including the rooftop solar and battery credit (§25D), home energy efficiency credit (§25C), and new home construction credit (§45L)-will all expire after 2025, removing federal support for distributed energy adoption.

- 30D (Clean Vehicles Credit): This credit will be repealed after 2026, with the 200,000-vehicle-per-manufacturer cap reinstated for Tax-Year 2026. Related credits for used EVs (25E) and commercial EVs (45W) will also be eliminated after 2025 for new projects.

- 45X (Advanced Manufacturing Credit): Begins a steep phase-down starting in 2027. Wind-related components are excluded entirely after 2028, and the credit is eliminated in full by 2031. Transferability is banned for components made after 2027.

- 45V (Clean Hydrogen Credit): Eligibility ends for any project not in service by December 31, 2025-impacting an estimated 95% of announced U.S. hydrogen capacity.

*OBBBA disqualifies wind and solar projects from receiving federal tax credits if deployed through residential leasing arrangements or third-party ownership models. Effective for tax years beginning after enactment (i.e., likely beginning with tax year 2026), this change eliminates eligibility under 25D for systems where the lessee, not the owner, would otherwise claim the credit, impacting common rooftop solar leasing and PPA structures.

Credits That Remain Intact (No Phase-Out)

Only three major IRA-era incentives remain broadly unaffected:

- 45Q (Carbon Capture Credit): Retains its current structure and full eligibility through 2032.

- 45Z (Clean Fuels Credit): Extended through 2031 but limited to U.S.-Mexico-Canada feedstocks and restricted by foreign entity bans (from 2026/2028) and transferability caps (after 2027).

- 45U (Zero-Emission Nuclear Power Production Credit): OBBBA preserves 45U in full throughout 2031, reversing the earlier proposal for a three-year phase-down. Notably, this credit applies only to existing nuclear power plants that qualify as “eligible advanced nuclear facilities” under Section 45U, defined as zero-emission facilities placed in service before the OBBA’s enactment.

The Case for New Nuclear Development

The OBBBA retains the 45U production tax credit for existing nuclear facilities through 2031 and includes a specific carve-out for new advanced nuclear projects to qualify for the tech-neutral 45Y/48E tax credits, as long as construction starts before 2029, with subsequent credit phase-out based on in-service years. To further support new nuclear development, President Trump signed a series of executive orders on May 23, 2025, launching a national strategy for expanding nuclear power. Building on provisions in the ADVANCE Act of 2024, these orders target key regulatory reforms-streamlining the Nuclear Regulatory Commission’s (NRC) licensing processes, accelerating the deployment of advanced reactor technologies, and revitalizing the domestic nuclear fuel cycle.

The executive orders establish specific goals: achieving 5 GW in uprates and constructing 10 new large reactors by 2030, with an overarching aim of increasing total nuclear capacity from 100 GW to 400 GW by 2050. While these directives emphasize regulatory acceleration, they do not introduce new tax credits for new reactors. Instead, they utilize provisions in the ADVANCE Act, including reduced licensing fees, financial prizes for first-mover projects, and risk-informed licensing for next-generation technologies such as Generation III+, Generation IV, small modular reactors (SMRs), and microreactors.

Whereas OBBBA narrows tax-based incentives to the existing fleet, the executive orders prioritize regulatory modernization and infrastructure readiness, positioning new nuclear as a long-term pillar of grid reliability in an evolving power sector.

Narrowing of Credit Transferability

Section 6418 of the IRA introduced the transferability of certain energy tax credits, allowing eligible entities to sell credits to unrelated parties. This was intended to enhance liquidity and expand access to tax equity financing. OBBBA retains the core transferability mechanism but imposes new constraints tied to compressed eligibility windows, substantially narrowing its value.

For the tech-neutral Production Tax Credit (45Y) and Investment Tax Credit (48E), transferability is preserved for the full credit period but only for projects placed in service by December 31, 2028. For 45U (nuclear PTC), transferability remains in place through its full eligibility window, with a placed-in-service deadline of December 31, 2031. This represents a tighter condition than earlier drafts, which had allowed transferability for projects that began construction up to two years after enactment.

Additional restrictions apply across other credits:

- 48 ITC (Geothermal): Transferability is repealed for projects that begin construction more than two years after the bill’s enactment.

- 45X (Advanced Manufacturing): Transferability ends for components sold after December 31, 2027.

- 45Z (Clean Fuels): Transferability ends for fuel produced after December 31, 2027.

Although the option to transfer credits remains in place, its effectiveness is significantly diminished by the compressed construction and in-service deadlines imposed by OBBBA. Developers who had planned to rely on multi-year monetization strategies enabled by the IRA now face a much narrower window, reducing the long-term value and flexibility that Section 6418 was originally intended to provide.

Expansion of Foreign Entity of Concern (FEOC) Restrictions

Beginning January 1, 2026, the OBBBA would prohibit energy tax credits from being claimed by any entity deemed to be controlled or influenced by a “Foreign Entity of Concern” (FEOC)-including those linked to China, Iran, North Korea, or Russia. This reflects an accelerated timeline from earlier drafts, which proposed a 2027 start. Critically, projects may also be disqualified if they receive “material assistance” from an FEOC, such as components, intellectual property, or design support. Given the extensive role of Chinese firms in the global supply chain for renewable energy materials and technologies, complying with these restrictions could pose significant challenges for many clean energy developers.

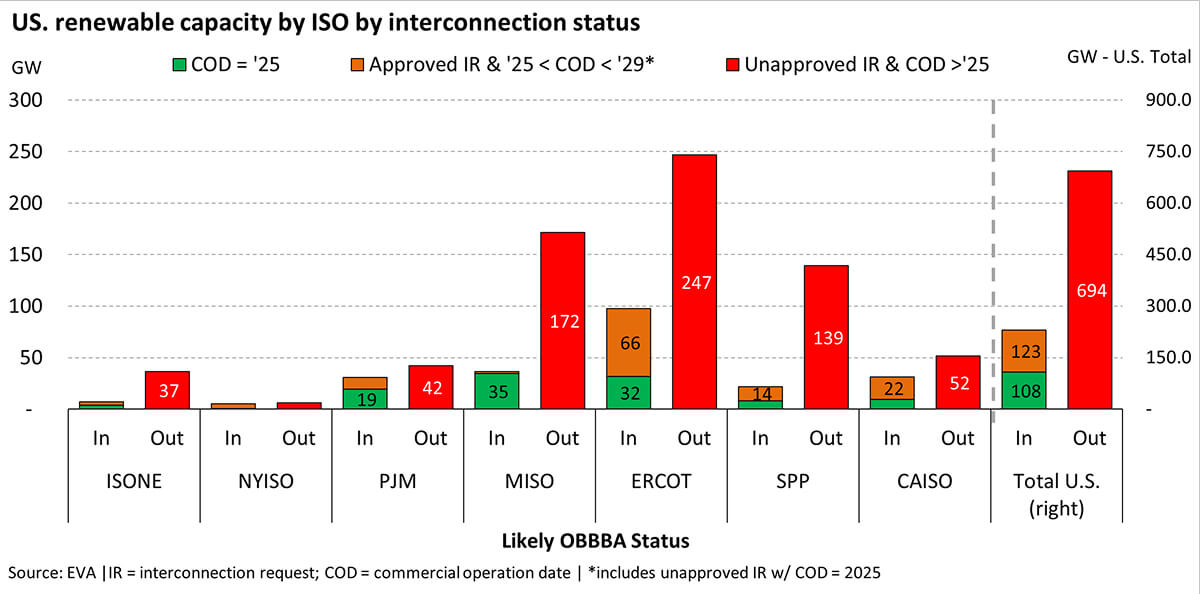

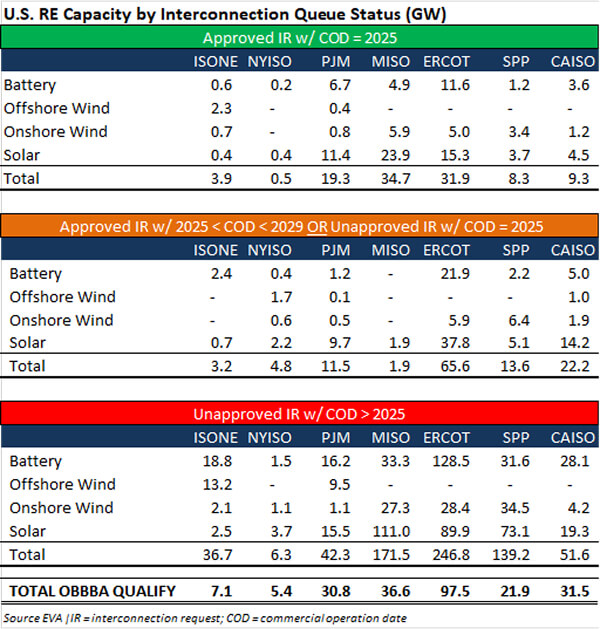

Disqualification Risks for the Broader Interconnection Queue

The OBBBA’s proposed 60-day “begin construction” trigger conflicts with the current state of interconnection backlogs. Despite efforts to streamline and cluster studies, interconnection continues to be a multi-year process, particularly for advanced technologies. OBBBA’s accelerated deadlines may disqualify shovel-ready projects that cannot feasibly overcome study and permitting obstacles in time, thereby undermining deployment and grid reliability objectives.

EVA analysis indicates that approximately 43 GW of clean energy capacity (solar, wind, and battery) with approved interconnection agreements could feasibly meet OBBBA’s dual eligibility thresholds in 2025. An additional 187 GW, with interconnection approval and commercial operation dates (CODs) between 2026 and 2028 or COD in 2025, has a possible path to qualification under the current construction and in-service deadlines. However, these estimates do not yet reflect potential reductions in buildout due to tariff risks or supply chain exposure to foreign entities of concern, which are also addressed under OBBBA. Regionally, markets like ERCOT, CAISO, and SPP stand out with the highest volume of approved projects, signaling relatively faster interconnection processing. In contrast, PJM and MISO face slower approval rates relative to the scale of their queue, limiting the number of projects that can reach construction readiness in time.

In stark contrast to the subset of qualifying projects, a vast share of the interconnection queue-approximately 700 GW across all seven major ISOs-will likely be disqualified from claiming any federal tax credits if OBBBA is enacted. This includes nearly 315 GW of solar, 258 GW of battery storage, and 121 GW of wind (both onshore and offshore). The most severely impacted regions by volume are expected to be ERCOT, MISO, and SPP, followed by CAIS and PJM, with the scale of exposure largely mirroring their requested queue capacity. These losses underscore the potential for widespread disruption to project financing and long-term planning across the U.S. renewables market.

Source: EVA

Source: EVA

Sector Implications

The combined provisions of OBBBA deliver a decisive policy shift across the clean energy ecosystem: New project development slows sharply, particularly for solar, wind, energy storage, and hydrogen facilities not already under construction or close to construction start. Investment risk increases since the loss of transferability and eligibility restrictions limit access to capital markets. Project cancellations are likely, with developers forced to reassess timelines and reconfigure supply chains under tight deadlines. Regional market prices may rise, particularly in capacity-constrained ISOs where renewable expansion was expected to relieve future stress.

At the same time, the elimination of distributed generation (DG) tax credits, such as for residential solar, could increase grid electricity demand as forecasted DG demand shifts back to utility-provided power. Yet, with new utility-scale clean energy deployments curtailed and new nuclear capacity years from coming online, planners face a near-term capacity gap. No new coal plants are under development, and gas turbine manufacturers face backlogs stretching into 2029, leaving few scalable options to offset the massive demand rise fueled by new data centers.

In response to the growing reliability concerns, the Trump Administration issued a series of key executive orders aimed at preserving existing dispatchable resources. In April 2025, a series of orders were passed aimed at extending coal plant operations, easing mining regulations, and challenging state-level emissions policies, potentially delaying more than 10 GW of coal retirements. While this may help address the near-term generation gap, the economic viability of such measures remains to be seen.

Conclusion

The One Big, Beautiful Bill Act (OBBBA) represents the most significant revision to U.S. clean energy policy since the Inflation Reduction Act. By establishing a stringent 60-day construction start rule, a 2028 in-service deadline, repealing major tax credits, and expanding restrictions on foreign-linked projects, OBBBA substantially narrows eligibility for federal energy incentives. These changes could reshape investment planning and slow the deployment of renewable energy, especially for projects still navigating lengthy permitting and interconnection processes.

Though advanced as part of a broader budget reconciliation effort, the bill may raise near-term energy costs and introduce new reliability risks, particularly in regions facing supply constraints. The rollback of distributed generation incentives could shift additional demand to the grid just as legacy coal capacity retires and new firm generation encounters multi-year procurement and permitting delays. With electricity needs accelerating due to data centers and AI adoption, the urgency for scalable, dispatchable supply is increasing. As policy shifts from expansive clean energy incentives to a more constrained, domestically-focused framework, long-term implications for energy competitiveness and infrastructure readiness remain uncertain.

While the bill awaits Senate consideration, its passage in the House indicates a shift toward prioritizing U.S. energy self-reliance by minimizing exposure to foreign supply chains. Developers, utilities, and investors may need to adapt their planning, financing, and procurement strategies in response to changes in credit eligibility, timelines, and the emphasis on domestic content and ownership. Furthermore, it remains uncertain how utilities will manage the balance between new demand connection requests and the limited supply options available over the next decade.

For a deeper understanding of how these developments impact the renewable energy landscape in various regions, explore EVA’s Monthly Renewable Energy Outlook, our comprehensive report on the U.S. renewable energy space. The marquee report offers unparalleled insights into policy, regulatory, and technological trends, helping stakeholders navigate the complexities of clean energy expansion.

To subscribe, request a sample, or for more information, please email us at [email protected]